CM Cost

CM cost—short for Cut‑Make cost—is basically what it takes a factory to turn raw materials into a finished garment. Not the fabric. Not the trims. Just the making part.

It covers things like:

- Cutting labor

- Sewing labor

- Finishing work

- General production overheads

That’s the money a factory earns (and survives on) to actually run the operation and hopefully make a margin.

And just to be clear—CM does not include:

- Fabric cost

- Trims and accessories

- Washing

- Printing or embroidery

- Export or commercial costs

Those sit elsewhere. CM is purely about production effort.

Why SMV‑Based CM Calculation Matters

Some factories still estimate CM based on experience or rough guesses. Sounds quick… but it usually backfires.

Using SMV-based CM calculation keeps things grounded.

- You get more accurate costing

- Buyer discussions become clearer (less back-and-forth)

- Easier to see where efficiency is slipping

- Helps reduce cost—if methods improve

- Keeps consistency across different styles

Without this system, small losses go unnoticed. And over time, those small gaps add up.

SMV

SMV (Standard Minute Value) is the time (in minutes) required for a skilled operator to perform a specific operation at standard environment, including allowances.

Nothing fancy. Just realistic time measurement.

But it drives a lot:

- Line balancing

- Capacity planning

- Efficiency tracking

- CM costing

Get the SMV wrong… and everything built on top of it starts to wobble.

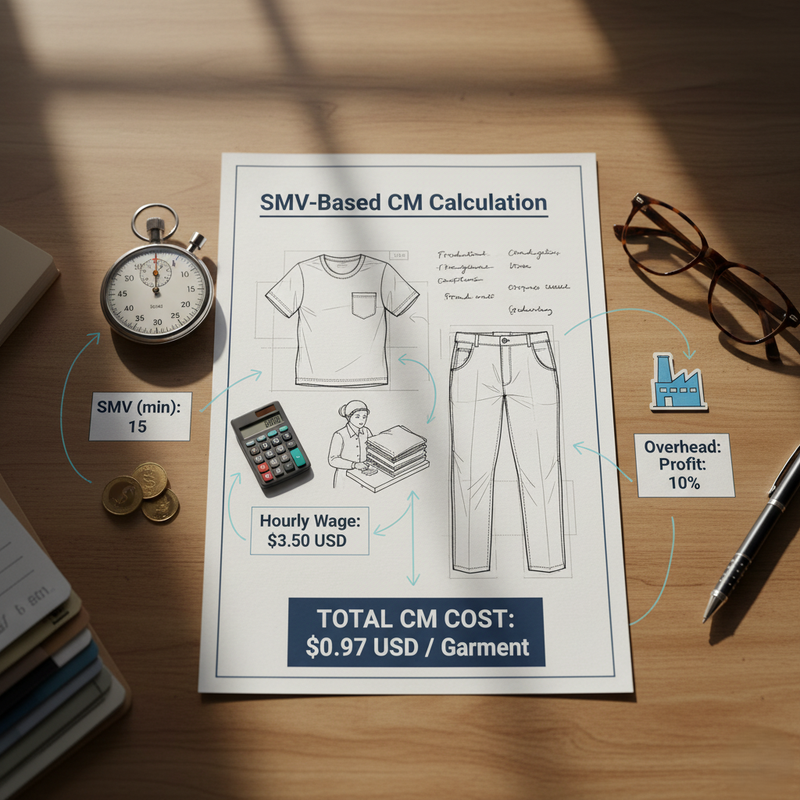

Core Formula for SMV‑Based CM Calculation

The standard industry formula is:

CM = (SMV × Labor Cost per Minute) ÷ Line Efficiency

Each element of this formula must be correctly calculated.

SMV‑Based CM Calculation Process flow

Step 1: Calculating Garment SMV- Operation Breakdown

First, the garment is broken into individual sewing, cutting and finishing operations.

Example: Basic Polo Shirt (Sewing Only)

| Operation | SMV (min) |

|---|---|

| Collar attach | 2.2 |

| Placket attach | 1.8 |

| Shoulder join | 0.6 |

| Sleeve attach | 2.5 |

| Side seam | 1.3 |

| Hem | 1.1 |

Total Sewing SMV = 9.5 minutes

Add:

- Cutting SMV ≈ 1.5 min

- Finishing SMV ≈ 2.0 min

Total Garment SMV = 13.0 minutes

Step 2: Calculating Labor Cost per Minute

Labor cost per minute depends on operator wage, working hours and factory payroll structure.

Example Calculation

- Average operator salary = USD 180 / month

- Working days = 26 days

- Working hours per day = 8 hours

Total working minutes per month:

26 × 8 × 60 = 12,480 minutes

Labor cost per minute:

180 ÷ 12,480 = USD 0.0144 per minute

Step 3: Line Efficiency Consideration

Efficiency measures how effectively working minutes are converted into production output.

Typical efficiency ranges:

- New style / complex item: 45–50%

- Regular style: 55–65%

- Basic repeat item: 65–75%

Efficiency must be realistic, not target‑based.

Step 4: CM Calculation Example (Polo Shirt)

Inputs:

- Total SMV = 13.0 minutes

- Labor cost per minute = USD 0.0144

- Line efficiency = 55% (0.55)

CM Calculation

CM = (13.0 × 0.0144) ÷ 0.55

CM = 0.1872 ÷ 0.55

CM = USD 0.34

This USD 0.34 covers pure labor cost only.

Step 5: Adding Factory Overhead to CM

Factories apply overhead to cover:

- Supervisor salary

- Maintenance

- Utilities

- Administration

- Depreciation

Overhead is usually added as:

- Fixed amount per minute or

- Percentage uplift on labor CM

Example: Overhead Addition

- Overhead loading = USD 0.45 per garment

Final CM = 0.34 + 0.45 = USD 0.79

This is the CM price quoted to buyer.

SMV‑Based CM Example for Different Products

Example 1: Basic Knit T‑Shirt

SMV = 8.5 min

Labor cost/min = USD 0.014

Efficiency = 65%

CM = (8.5 × 0.014) ÷ 0.65

CM ≈ USD 0.18

Final CM (with overhead) ≈ USD 0.55

Example 2: Woven Shirt

SMV = 30.0 min

Labor cost/min = USD 0.014

Efficiency = 50%

CM = (30 × 0.014) ÷ 0.50

CM = USD 0.84

Final

CM ≈ USD 1.80–2.10

Example 3: Denim Pant

SMV = 52.0 min

Labor cost/min = USD 0.015

Efficiency = 48%

CM = (52 × 0.015) ÷ 0.48

CM ≈ USD 1.63

Final CM ≈ USD 3.00–3.80

Role of IE Team in SMV‑Based CM

The IE team sits right in the middle of all this. Not on the side. Not optional.

They’re the ones who actually build the numbers everyone else depends on.

- Running time studies to calculate SMV

- Looking at methods and asking, “can this be done better?”

- Balancing lines so work flows instead of bottlenecking

- Pushing for real efficiency improvements—not just targets on paper

If IE gets it wrong, CM gets shaky. Simple as that.

That’s why merchandising CM should never bypass IE validation.

It might feel faster in the moment, but it usually costs more later.

How Merchandisers Use SMV‑Based CM in Negotiation

On the merchandising side, SMV data becomes a tool. A pretty powerful one, actually.

Instead of guessing or pushing numbers blindly, they can:

- Justify price increases with actual work content

- Explain why one style costs more than another

- Negotiate based on efficiency improvements, program by program

- Protect margins—without damaging buyer relationships

And buyers notice this. When numbers are backed by logic (and data), discussions change tone.

Less arguing. More alignment.

Common Mistakes in SMV‑Based CM Calculation

Even with a solid system, things can go wrong. And they do.

Some of the usual slip‑ups:

Overestimating efficiency

(looks great on paper… falls apart on the floor)

Ignoring the learning curve

New styles never hit peak efficiency from Day 1

Using outdated SMVs

Methods change, machines change—numbers should too

Skipping finishing SMV

Easy to miss, but it adds up

Quoting CM too low

To win orders… and then struggling to deliver

These aren’t small issues.

They lead to production loss, extra pressure on operators, and eventually quality problems.

Benefits of SMV‑Driven CM Costing

When it’s done right, you start to see the difference.

- Accurate pricing → fewer surprises later

- Clear visibility → everyone understands where time is spent

- Sustainable margins → not just short-term wins

- Process improvement opportunities → gaps become visible

- Stronger buyer trust → because numbers actually make sense

Factories that stick to SMV-based CM tend to handle cost pressure better. They adjust. They improve. They survive longer.

Conclusion

SMV‑based CM isn’t just a calculation method—it’s basically the backbone of scientific garment costing.

It ties cost directly to:

- the actual work involved

- the efficiency you can realistically achieve

- and what the factory is truly capable of doing

No guesswork. Or at least, less of it.

In today’s apparel industry—where margins are tight and expectations are high—this matters more than ever.

Factories that really understand and use SMV-based CM don’t just quote better.

They plan better. Run better. And stay competitive when things get tough.